Infield Systems

provides a snapshot of the global flexible pipelines market up to 2019

In preparation for

Infield Systems’ new edition of its Pipeline and Control Lines market report,

due for release June 2015; Infield Systems provides a snapshot of the global flexible

pipelines market up to 2019.

Latin America, Africa, Europe and Australasia are all

expected to see increases in flexible pipeline investment over the next five

years in comparison to the historic period (2010-2014).

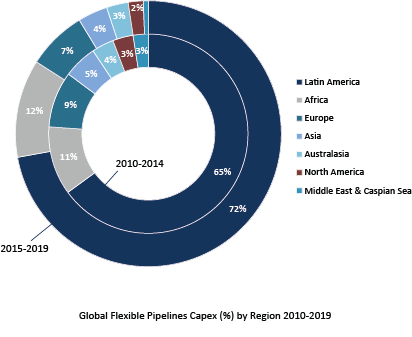

Latin America will continue to dominate the the flexible

pipelines market, with the region accounting for over 69% of global flexible

pipeline installed over the next five years. Brazil is the principle driver of

the regions flexible demand, which could account for around 98% of Latin

American flexible pipeline Capex between 2015 and 2019. Brazil has large

offshore reserves, a significant proportion of which are located in deep and

ultra-deepwaters which is a key driving force behind the use of flexible lines

in the country. Petrobras will continue

to have the highest demand, with its ultra-deepwater Iracema North oil field

anticipated to require the largest amount of flexible pipeline investment over

the forthcoming period.

|

|

Africa’s demand for flexible pipelines expenditure could

increase by 57% and 87% in projected length installed in comparison to the

historic period, with West Africa expected to be the mainstay of demand. The

two largest offshore African markets, Angola and Nigeria could together account

for 55% of the regions flexible pipeline Capex demand. Total’s ultra-deepwater

Egina project in Nigeria is expected to see the largest amounts of flexible

pipeline investment over the next five years.

European demand for flexible pipelines could increase by 16%

in terms of Capex demand and 30% in projected length installed in comparison to

the historic period. Demand will continue to be centred on projects in North

West Europe, mainly associated with the UK and Norway, which are the key driver

of offshore oil and gas activity in the region. Chevrons Rosebank field in the

UK could see the highest levels of flexible pipeline investment, most of which

will be focused towards flowlines.

Australasia’s flexible pipelines expenditure could increase

by 7%. The vast majority of the region’s demand will continue to be focused on

Australia which is the regions hub of offshore oil and gas activity. Australian

Independent Woodside is anticipated to inject the most in to the regions

flexible pipelines market, with its Laverda field in the Greater Enfield Area

potentially a key driver of the operators demand.

|

Asia, North America and the Middle East and Caspian Sea

regions may see a decline in flexible pipeline expenditure over the next five

years in comparison to the historic period. The decrease in Capex in the Middle

East is largely associated with the completion of Manavgat’s Turkey – Cyprus

water pipeline, and the reduction in flexible pipeline demand associated with Saudi

Aramco Kuwait Gulf Oil’s Khafji oil field in the Neutral Divided Zone. Asia’s

demand for flexible pipelines could decrease by 3% in terms of Capex demand

mainly due to a potential fall in demand in India. The fall in North American

flexible pipeline expenditure is mainly a result of an expected fall in investments

in the US Gulf of Mexico due to the completion of a number of fairly high cost

flexible pipeline projects such as during the historic period such as LLOG’s Who

Dat oil field and Anadarko’s Lucius oil field.

In summary, the global flexible pipeline market is expected

to see an increase in expenditure, with Brazil continuing to be a massive

demand driver. Africa is may see large increases in flexible demand, mainly

fuelled by West African developments, with East African developments expected

to support Africa’s demand towards the end of the forecast.